Cash Reserve Ratio = CRR 👈 👉 SLR = Statutory Liquidity Ratio

In the previous post, we read about the Monetary Policy Committee (MPC) and the instruments of the monetary policy. The RBI uses instruments of the monetary policy to regulate the price stability in the economy.

The Cash Reserve Ratio (CRR) and the Statutory Liquidity Ratio (SLR) are among the monetary policy instruments. The increase or decrease in these ratios influence the banking sector’s lending capacity. As per RBI mandate, commercial banks must maintain a percentage of their liabilities as cash. And must maintain a percentage of the liabilities as liquid assets.

What is an asset ➡️ An asset is something that has a value, and an individual or an institution owns it. An asset has a potential to provides us some economic benefits. E.g. cash, real estate property, an investment. It can be a non-physical thing, like a patent, a knowledge, relationships, etc.

Meaning of liability ➡️ A liability is an obligation or debt that we need to pay to someone. A liability do not generate us any profits/benefits. E.g. a loan, issuing a bond, buying on credit, etc.

From a bank’s perspective, the assets and liabilities are –

- Assets = office building of a bank (if that bank owns it), loans given to their customers, interest accrued on loans, machines, computers, etc.

- Liabilities = rent of office building (as bank doesn’t own it), deposits of the customers in that bank (both demand and time deposits), loan taken by a bank from the RBI or any other loan, etc.

What is CRR and SLR ?

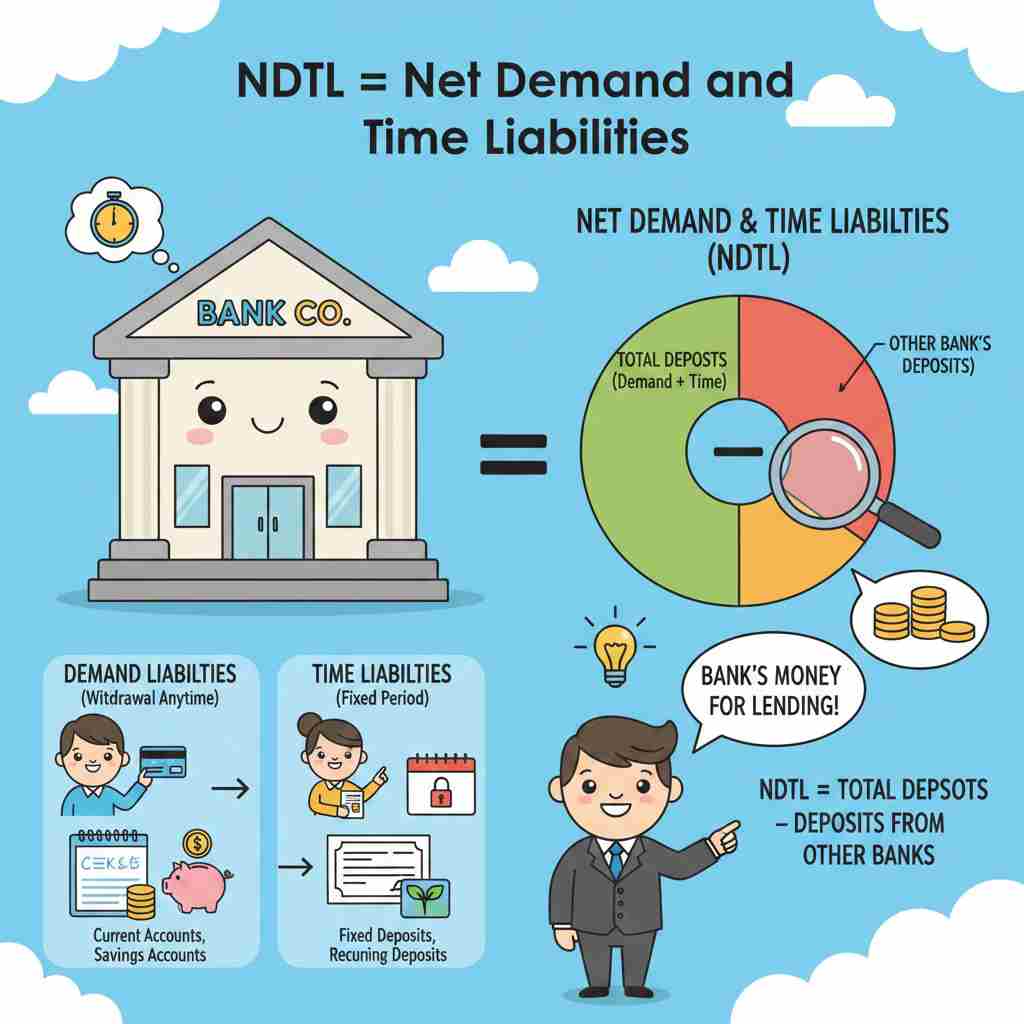

Before understanding CRR and SLR, we need to understand the Net Demand and Time Liabilities (NDTL) of a bank. The NDTL is the net value of the total assets minus total liabilities of a bank. It decides the CRR and SLR calculations. It is the value of a bank’s liability and not the assets.

Read in detail about 👉 RBI – CRR & SLR

NDTL

The Formula, NDTL = (Demand liabilities + Time liabilities) – (Deposits of a bank with the other banks)

- Demand liabilities =

- deposits of customers in Savings and Current accounts. Can withdraw money at ant time.

- Time liabilities =

- deposits of customers in fixed deposits (FDs) and other schemes that have a maturity period.

- Deposits of a bank with other banks =

- A bank keeps deposits it another bank to manage liquidity problems and payment settlement, etc.

Let’s understand this with the help of an example –

Imagine a bank that has only one savings account and only one current account. The same bank has only one FD (fixed deposit) account. To calculate the Net Demand and Time Liabilities (NDTL) of this bank, we need to put some money as deposits into the bank.

The savings account has Rs.5000, the current account has Rs.10000 and someone has the FD of Rs.100000 in the bank. And the same bank has its funds/money placed in another bank, which is around Rs.20000.

By putting these values in the formula of NDTL –

NDTL = (Demand liabilities + Time liabilities) – (Deposits of a bank with the other banks)

= (5000+10000 + 100000) – (20000)

= 115000 – 20000

NDTL= 95000 Rupees.

The bank has NDTL of Rs.95000 as per the example.

Now, we have understood the concept of NDTL. NDTL decides the amount which a bank can lend, with some compulsory reserves maintained with the RBI. CRR and SLR are the reserve ratios that a bank must maintain with the RBI to cope with emergency liquidity crisis.

The CRR and SLR are calculated as a percentage of a bank’s NDTL.

- The current percentage of CRR is 4.5% of a bank’s NDTL (December 2025).

- The SLR is 18% of a bank’s NDTL (December 2025).

The RBI may change these ratios as per the economic, financial and monetary conditions.

CRR (Cash Reserve Ratio)

CRR is a reserve of only cash, which is mandated to be placed with the RBI. The Cash Reserve Ratio, as the name suggests, requires a bank to maintain a percentage of its deposits in the form of cash. A bank cannot lend this cash to anybody. The CRR is usually around 4% and is changed from time to time by the RBI.

This reserve helps a bank in the situation of a ‘Bank Run’. Bank run is an emergency situation where most of the customers withdraw their deposits simultaneously due to some fear or news, etc. In such emergency situations, CRR reserves help that bank to cool the situation.

SLR (Statutory Liquidity Ratio)

The concept of liquidity means how fast an asset can be converted into cash without loosing its significant market value. Cash is the most liquid asset. Gold is more liquid than a bond or a government security paper. A real estate property is less liquid than a short-term bond or gold.

Statutory Liquidity Ratio reserves contains government securities, gold, RBI approved securities. It also contains cash as an asset.

How RBI uses these ratios ?

The Reserve Bank of India (RBI) uses these reserve ratios as monetary policy tools. The central bank manages and influences the liquidity of the banking sector through CRR and SLR.

- When there is high liquidity in the economy, the RBI increases the CRR and SLR. Increasing these ratios mandates banks to maintain more money and assets as reserves, and banks are left with less money to lend. This reduces the money in circulation.

- The high inflation rate in the economy prompts the Reserve Bank of India to increase these reserve ratios. When the CRR and SLR increase, the money in the system automatically decreases because banks have less money to lend.

- The reverse in done by the RBI when the liquidity is quite low. The central bank reduces the CRR and SLR in case of low cash/money in the system, or when there is recession/very low inflation rate.

These reserve ratios help the RBI to manage the liquidity of the banking system quite efficiently. CRR and SLR ratios also help banks to mitigate emergency crises like bank runs. By keeping such safety reserves, the banking system and the central bank keep the confidence of the people alive in the banking and financial system of the country.