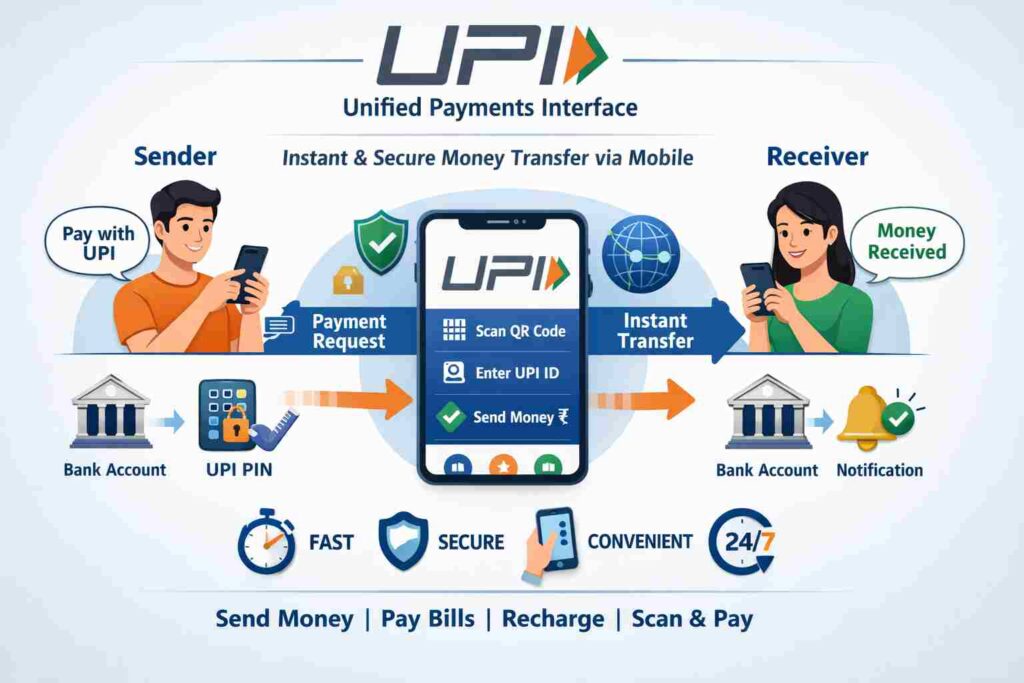

The Unified Payments Interface (UPI) is India’s online payments system. UPI lets you transfer money online directly into a bank account linked to the UPI. NPCI (National Payments Corporation of India) launched it in 2016.

Money is a medium of exchange through which we can buy and sell things. One of our articles discusses the evolution of money, reading that article one can learn how we have progressed from the barter system to the new age online payment systems.

Cash is the most used payment method across the world, as it is the most liquid asset. And people prefer it by choice.

Dealing with physical money presents challenges, including the risk of theft, damage due to liquid, and the possibility of tearing.

Cash payments are not transparent as compared to card or online payments. Keeping all these things in mind, the NPCI brought the revolutionary initiative – the UPI system.

Unified Payments Interface (UPI)

What is UPI (Unified Payments Interface) –

The UPI is India’s instant online payment system developed by the NPCI. UPI lets you send and receive money in a bank account using an app (UPI app). It works 24×7 and connects multiple bank accounts in one app. UPI is popular because of its user-friendly interface, and it is quite easy to use, even for a layman.

Source = NPCI website

NPCI (National Payments Corporation of India)

National Payments Corporation of India is an entity under the RBI (Reserve Bank of India) regulation. It is an initiative of the RBI and the Indian Banks’ Association (IBA) for creating a retail payment infrastructure in India. NPCI comes under the Payments and Settlement Systems Act, 2007. In 2008 this organization started its working.

It is a not-for-profit company registered under the Companies Act, 2013. The goal of the NPCI is to provide an accessible and affordable payments and settlement system to the entire banking system.

The IMPS

The immediate payments system (IMPS) is India’s instant real time money transfer online system developed by the NPCI. It is accessible via mobile banking, internet banking, ATMs and even with SMS. It is used for the transfer of payments higher than the UPI limit.

Difference between UPI and IMPSNo

The UPI is more user-friendly and popular for retail payments. While IMPS is useful for larger transactions.

| Feature | IMPS (Immediate Payment Service) | UPI (Unified Payments Interface) |

|---|---|---|

| Identifier | Account Number and IFSC Code | Virtual Payment Address (VPA), Mobile Number, or QR Code or UPI ID. |

| Use Case | Primarily bank-to-bank fund transfer. | Comprehensive ecosystem: P2P (person to person), merchant payments (QR), bill pay, auto-debits, IPOs. |

| Setup | Requires payee registration with bank details. | Instant setup via VPA; can link multiple accounts in one app. |

| Convenience | Less convenient due to detailed info needed. | Highly convenient, mobile-first, simple IDs. |

| Access | ATMs, Net Banking, Mobile Banking. | Mobile Apps (Google Pay, PhonePe, etc.). |

| Limits | Higher limits (e.g., ₹2L-₹5L), bank-dependent. | Lower daily limit (₹1L), bank-dependent. |

| Features | Basic fund transfer. | Request money, split bills, scan & pay, auto-pay. It comes with more features and it is more convenient than the IMPS. |

10 Facts about the Unified Payments Interface

The UPI is a game-changing technology for our economy. It boosted the process of financial inclusion in India. Its easy-to-use features are at the center of its success, and no other country in the whole world has ever achieved the number of online transactions that we witness on a daily basis.

- 1. Nearly half of the world’s digital payments are done using the Unified Payments Interface (UPI).

- India accounts for the 49-50% of all the online payments done globally!

- 2. UPI is not just limited to India, the technology has already crossed the borders and many other countries started using it.

- France, UAE, Singapore, Qatar, Nepal, Bhutan, etc.

- 3. The Unified Payments Interface is the largest and number one ‘real-time payments system’ in the world (by volume = by the number of transactions).

- Its average is 60 to 70 crores transaction per day. It holds the record for the highest number of transactions in a single day with 75.4 crore transactions on 18 October 2025 (Diwali)🎇🧨🪔.

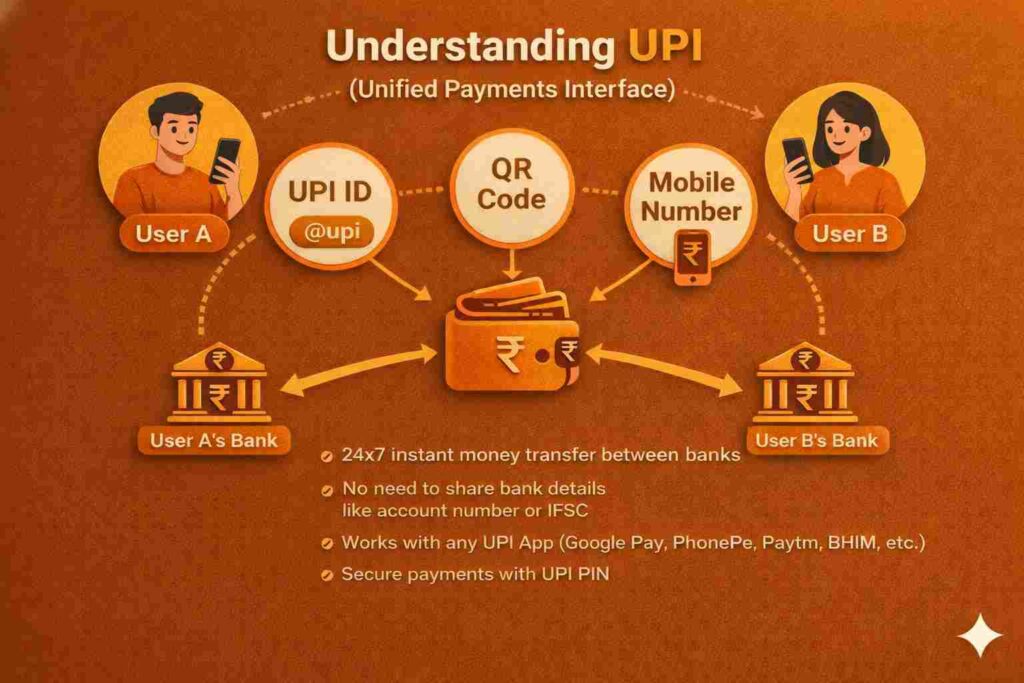

- 5. No bank details are required for each transaction. One can use mobile number or unique QR code or UPI ID to send and receive money instantly.

- This thing insures your safety and privacy.

Read about the RBI

- 6. It is easy to send money using a UPI app to another UPI app without any extra fees or filling other details.

- As each app uses the same technology developed by the NPCI.

- 7. UPI has digitized the entire payments system, from big merchants to small businesses like street vendors, coconut sellers, tea stalls, etc.

- 8. You can now link your RuPay credit card to UPI, it allows you to pay using your credit limits.

- 9. UPI is a digital good which is free of cost in most cases, as the Government of India promoted it. The user-friendly interface is also a major reason for its rapid adaptation in India and abroad.

- 10. The standard daily limit (24 hours) for UPI transactions is 1 lakh rupees. But the RBI has increased this limit for specific sectors like hospital bills, educational institutions, etc. It ensures that UPI remains a viable option in case of an emergency payment.